Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Looking ahead to 2025, it’s important to know what experts are projecting for the housing market. And whether you’re thinking of buying or selling a home next year, having a clear picture of what they’re calling for can help you make the best possible decision for your homeownership plans.

Here’s an early look at the most recent projections on mortgage rates, home sales, and prices for 2025.

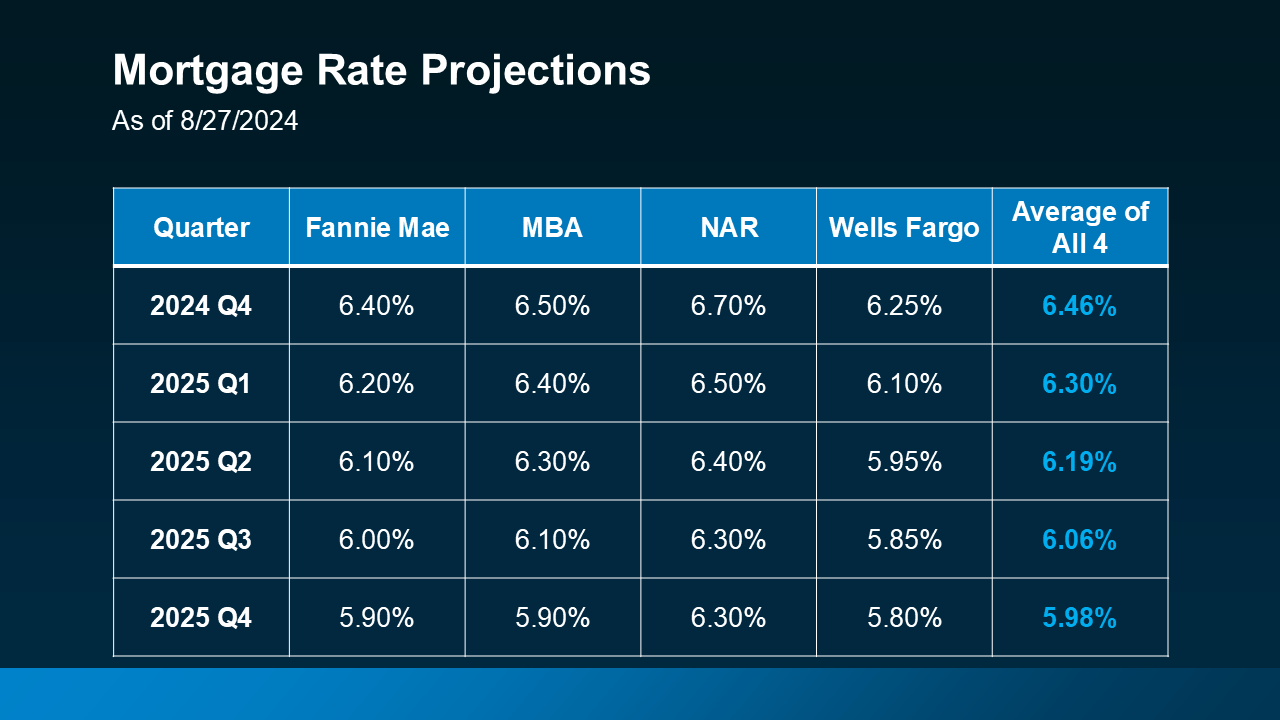

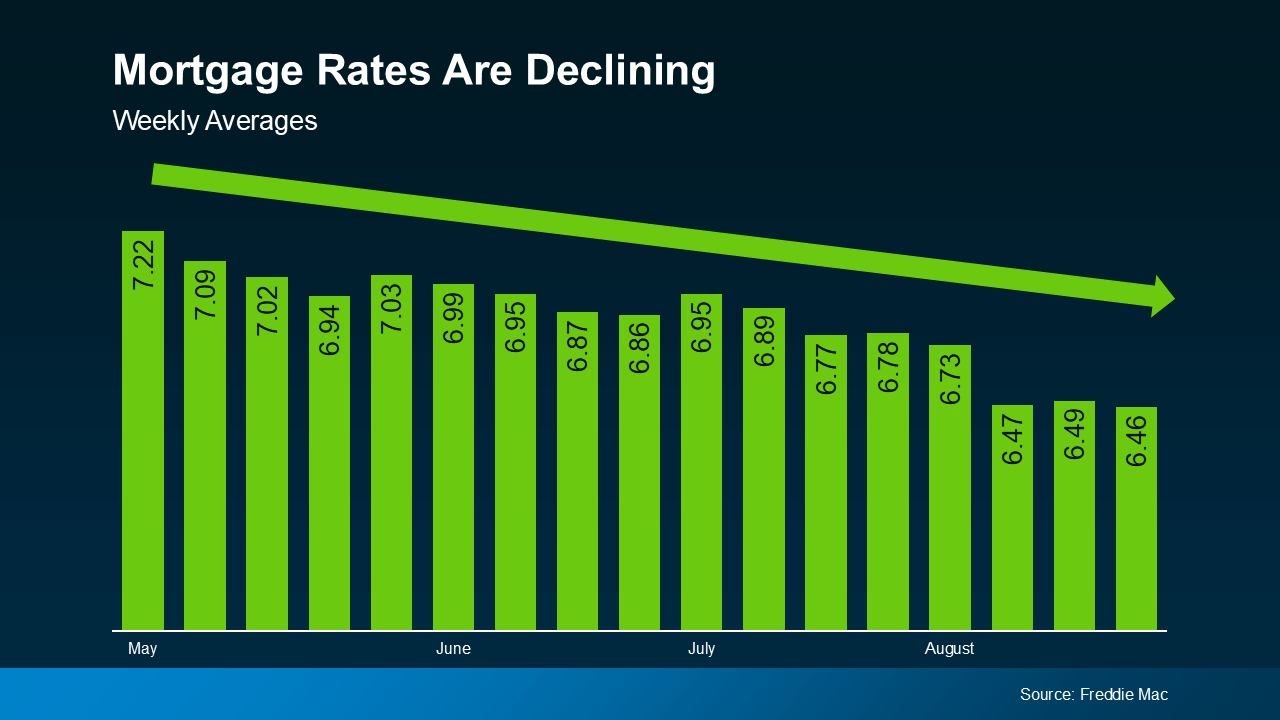

Mortgage Rates Are Projected To Come Down Slightly

Mortgage rates play a significant role in the housing market. The forecasts for 2025 from Fannie Mae, the Mortgage Bankers Association (MBA), the National Association of Realtors (NAR), and Wells Fargo show an expected gradual decline in mortgage rates over the course of the next year (see chart below):

Mortgage rates are projected to come down because continued easing of inflation and a slight rise in unemployment rates are key signs of a strong but slowing economy. And many experts believe these signs will encourage the Federal Reserve to lower the Federal Funds Rate, which tends to lead to lower mortgage rates. As Morgan Stanley says:

Mortgage rates are projected to come down because continued easing of inflation and a slight rise in unemployment rates are key signs of a strong but slowing economy. And many experts believe these signs will encourage the Federal Reserve to lower the Federal Funds Rate, which tends to lead to lower mortgage rates. As Morgan Stanley says:

“With the U.S. Federal Reserve widely expected to begin cutting its benchmark interest rate in 2024, mortgage rates could drop as well—at least slightly.”

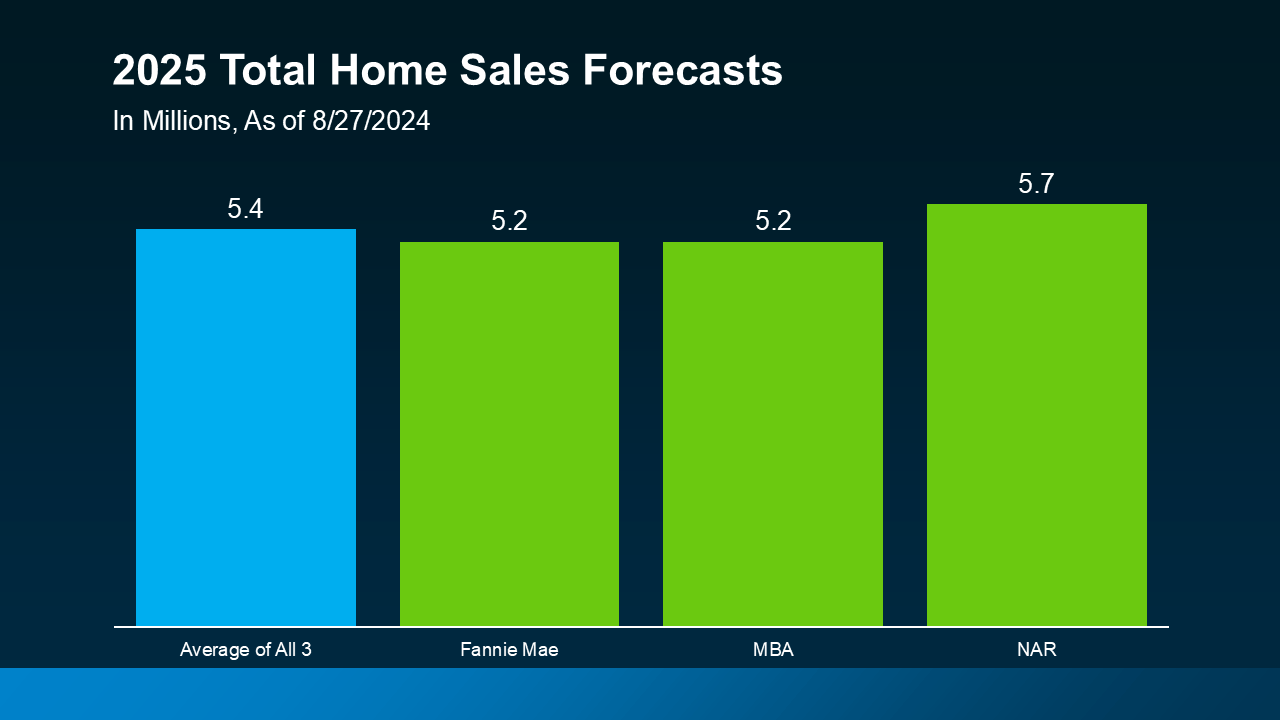

Expect More Homes To Sell

The market will see an increase in both the supply of available homes on the market, as well as a rise in demand, as more buyers and sellers who have been sitting on the sidelines because of higher rates choose to make a move. That’s one big reason why experts are projecting an increase in home sales next year.

According to Fannie Mae, MBA, and NAR, total home sales are forecast to climb slightly, with an average of about 5.4 million homes expected to sell in 2025 (see graph below):

That would represent a modest uptick from the lower sales numbers in 2023 and 2024. For reference, about 4.8 million total homes were sold in 2023, and expectations are for around 4.5 million homes to sell this year.

That would represent a modest uptick from the lower sales numbers in 2023 and 2024. For reference, about 4.8 million total homes were sold in 2023, and expectations are for around 4.5 million homes to sell this year.

While slightly lower mortgage rates are not expected to bring a flood of buyers and sellers back to the market, they certainly will get more people moving. That means more homes available for sale – and competition among buyers who want to purchase them.

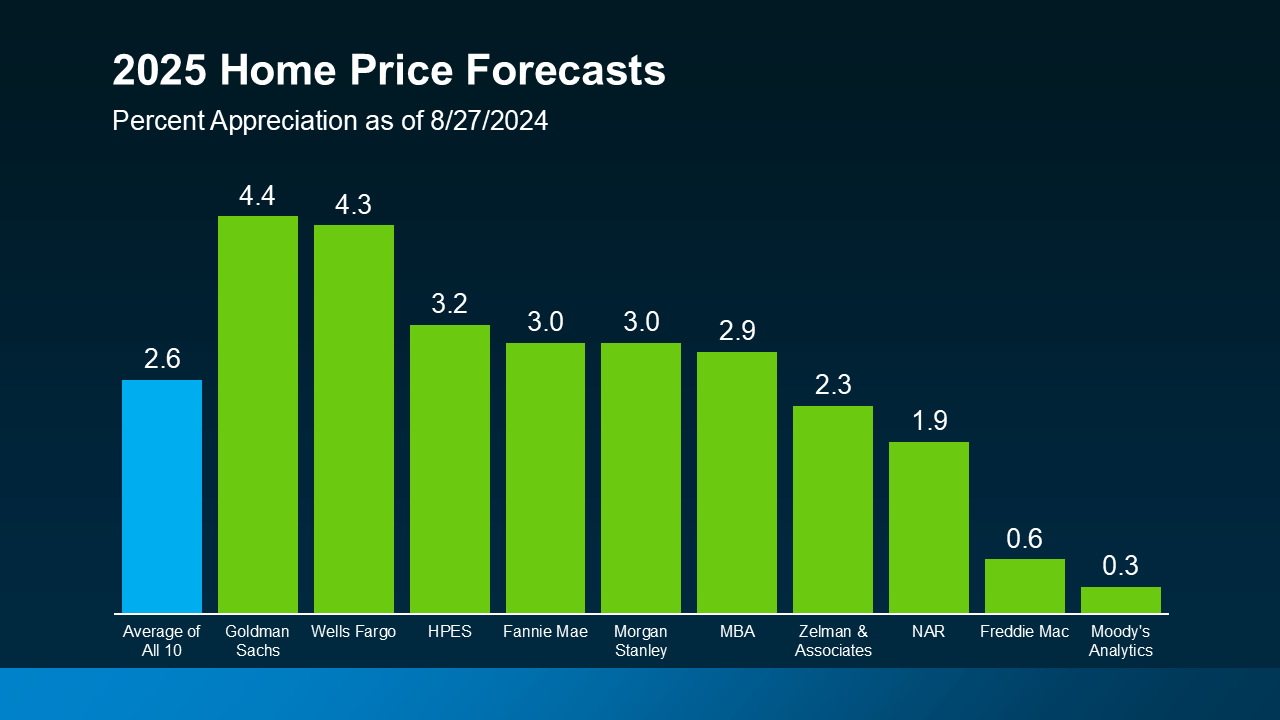

Home Prices Will Go Up Moderately

More buyers ready to jump into the market will put continued upward pressure on prices. Take a look at the latest price forecasts from 10 of the most trusted sources in real estate (see graph below):

On average, experts forecast home prices will rise nationally by about 2.6% next year. But as you can see, there’s a range of opinions on how much prices will climb. Experts agree, however, that home prices will continue to increase moderately next year at a slower, more normal rate. But keep in mind, prices will always vary by local market.

On average, experts forecast home prices will rise nationally by about 2.6% next year. But as you can see, there’s a range of opinions on how much prices will climb. Experts agree, however, that home prices will continue to increase moderately next year at a slower, more normal rate. But keep in mind, prices will always vary by local market.

Bottom Line

Understanding 2025 housing market forecasts can help you plan your next move. Whether you’re buying or selling, staying informed about these trends will ensure you make the best decision possible. Let’s connect to discuss how these forecasts could impact your plans.

Let’s Talk Soon!

2. How Many Jobs the Economy Is Adding

2. How Many Jobs the Economy Is Adding